Who Will Stop Amazon?

Who Will Stop Amazon?

Amazon Due Diligence [1/3]

Dear investor,

As you probably know, Jeff Bezos stepped down as Amazon CEO on Monday - July 5th, exactly 27 years after he founded the company. During these 27 years, business results have been extraordinary, and I’m convinced that shareholders are more than satisfied with the obtained returns.

Here you have a summary of how the main financial metrics have evolved during the last 27 years (1995-2021)

Revenues went from $511 thousand to $419 billion -> CAGR: 84.5%

EBITDA went from negative $285 thousand to $57 billion.

Net income went from negative $303 thousand to $27 billion.

Free Cash Flow went from negative $284 thousand to $22 billion.

Operating margins improved from negative 59% to positive 7%.

Cash reserves went from $6,248 thousand to $73 billion.

As you can see, the growth in all the financial aspects of the business is astonishing, and no shareholder who had invested in Amazon from the beginning could have predicted this evolution.

At the same time, $10,000 invested Amazon.com during its IPO (May 1997) at $16.00 per share, today would be worth $2,330,000 or 233 times your initial investment, which means an annual return of 25% during 25 years, assuming no shares were sold during this period. Easier said than done!

Many of you asked me to write an article about Amazon similar to that I wrote about Facebook some time ago. If you want to review my analysis of Facebook you can do it here -> 12 Reasons to Buy Facebook Stock and Never Sell

Both are amazing companies, and it’s always good to perform business analysis regardless of the valuation. When I wrote about Facebook I considered its valuation was attractive, and from my point of view the stock was undervalued at the time of the analysis. That might not be the case today with Amazon. Investors should perform their due diligence, think independently, and draw their own conclusions.

This post will be the first part of a series of three articles that will be published in the next few weeks.

Currently, Amazon represents close to 7% of my portfolio, and I have no intention of selling the stock anytime soon.

Having said that, let’s get started!

Business Strategy and Outlook

Amazon dominates its served markets, notably for e-commerce and cloud services. It benefits from numerous competitive advantages and has emerged as the clear e-commerce leader given its size and scale, which yield an unmatched selection of low-priced goods for consumers.

The secular drift toward e-commerce continues unabated with the company continuing to grind out market share gains despite its size. Prime ties Amazon’s e-commerce efforts together and provides a steady stream of high-margin recurring revenue from customers who purchase more frequently from Amazon’s properties. In return, consumers get one-day shipping on millions of items, exclusive video content, and other services, which result in a powerful virtuous circle where customers and sellers attract one another.

The Kindle and other devices further bolster the ecosystem by helping attract new customers, while making the value proposition irresistible in retaining existing customers. Through Amazon Web Services (AWS), Amazon is also a clear leader in public cloud services.

Additionally, the firm’s advertising business is already large and continues to scale, thus offering an attractive option for marketers looking to access a vast audience with a variety of proprietary data points about those very consumers. AWS, advertising, and subscriptions are growing faster than e-commerce except for the 2020 spike in online shopping.

These three areas are expected to be the main growth drivers over the next several years. This is critical, as each of these segments drives higher margins than the corporate average, which in turn should allow both operating profit and earnings per share to outgrow revenue as margins continue to expand.

It seems difficult to discover something new in Amazon, but the reality is that there is a lot to discover. If you perform a deep business analysis you will realize that most segments are in their early stages. Overall, I see strong revenue and free cash flow growth for years to come.

A Diverse Revenue Model

With a market cap of $1.9 trillion, Amazon is currently the most valuable retailer in the world and the third U.S largest company behind Apple and Microsoft.

Amazon is a company that has always had a long-term focus. This means that since its inception, it has renounced short-term profitability to become one of the most important companies in the world in the long term. Without any doubt, Amazon has achieved this goal, and currently is collecting what has been settled for so many years.

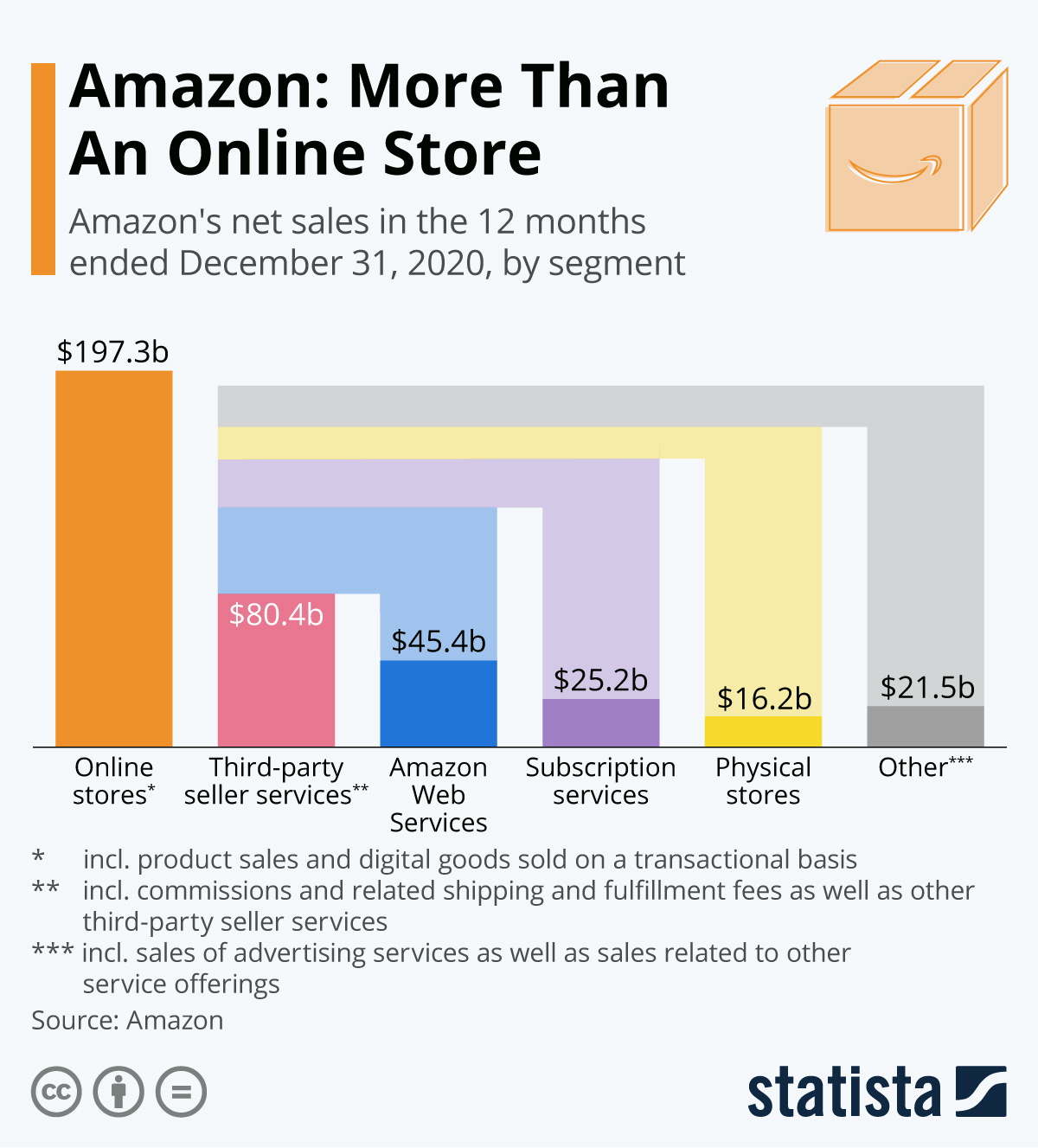

A key factor in the company’s success is its diversification into other areas. Here’s a breakdown of Amazon’s revenue mix:

Retail Sales

Amazon is the world's largest online marketplace as measured by revenue. Thanks to this user experience created by Amazon, it has been one of the main contributors (or rather the main contributor) to the explosive evolution of e-commerce, making its penetration increasingly higher and its growth very high.

Worldwide retail e-commerce sales of Amazon from 2017 to 2021(in billion U.S. dollars)

Source: Statista

According to Statista data, e-commerce penetration worldwide is 51% in 2021 and is expected to reach 63% in 2025. Average spending per person exceeds $700 per year. Between 2020 and 2025, e-commerce revenues are expected to grow by 50%. We still can see some strong growth coming ahead.

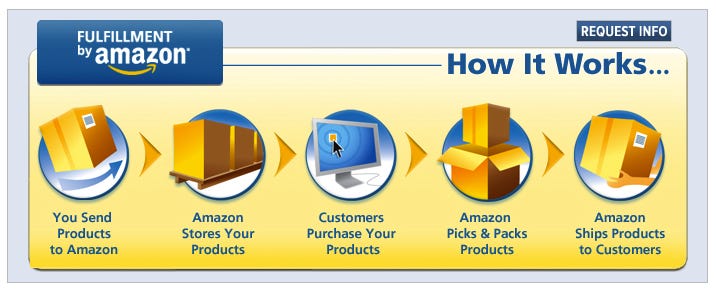

Fulfillment by Amazon (FBA)

More than half of the units purchased on Amazon's global marketplaces are sold by third-party merchants: sellers large and small who benefit from having access to Amazon's millions of customers.

Fulfillment by Amazon (FBA) is a program that allows sellers to ship their inventory to Amazon's distribution centers, where they create, pack, and ship orders for them, as well as handle customer service and returns for them. Their products become part of the Prime program, so they reach an even larger audience, and the seller spends fewer resources on inventory management and shipping.

The fulfillment segment benefits from operational leverage, managing to contain unit costs, and generating a higher free cash flow when the business scales.

Amazon has been investing in its fulfillment network for many years, reinforcing its increasingly evident MOAT regarding logistics capacity and customer experience.

The company is already competing against rival companies, which their core business is precisely that.

Source: Annual reports & Own elaboration

As you can see in terms of fulfillment capacity Amazon has the highest capacity comparing with other well-established businesses in the shipping industry. However, in terms of the number of vehicles and aircraft, Amazon is below UPS and FedEx.

With the scale that the business has acquired, it would not be unreasonable for Amazon to own a more efficient logistics platform than other traditional players in the shipping industry in the coming years.

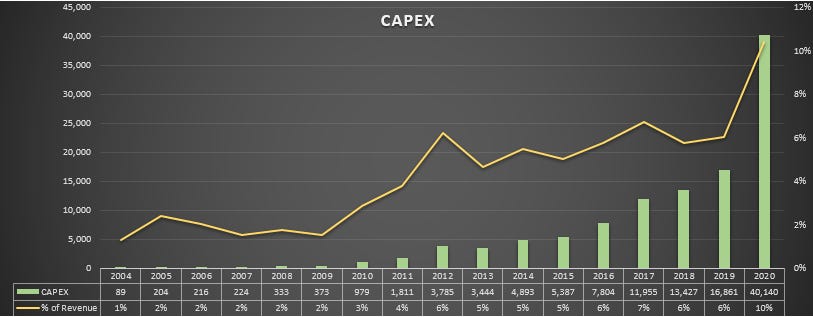

Today Amazon has more than 1,600 fulfillment centers, and most of them were built recently in 2020. Fulfillment centers require big investments of Capex, and as you can see Capex investments for the year 2020 were higher than usual. Of course, not all Capex investments are related to fulfillment centers, but it is clear that a large part of capital investments are associated with Amazon FBA.

Source: Own elaboration

This investment in Capex is reflected in the evolution of the square meters of fulfillment. From 2010 to 2020, total fulfillment square footage increased from 25,000 to 389,000.

In addition, Amazon is also increasing its aircraft fleet, which started in 2016. Currently, the fleet of aircraft under a lease is 82 plus 11 owned aircraft, a total of 93. In 5 years, it has more than doubled the fleet. These movements make clear Amazon's intentions to boost the air service.

The current gap in the number of aircraft comparing with UPS and FedEx is significant. However, if Amazon keeps investing high amounts of capital in fulfillment development, the company could achieve a similar fleet to that of UPS and FedEx during the next years.

It seems likely that in the coming years, Amazon would be able to undercut third-party carriers by leveraging the capacity already used for its deliveries. This is a key point, as Amazon bets more on its shipping infrastructure and less on third parties, it will acquire a higher gross margin and reduce added costs.

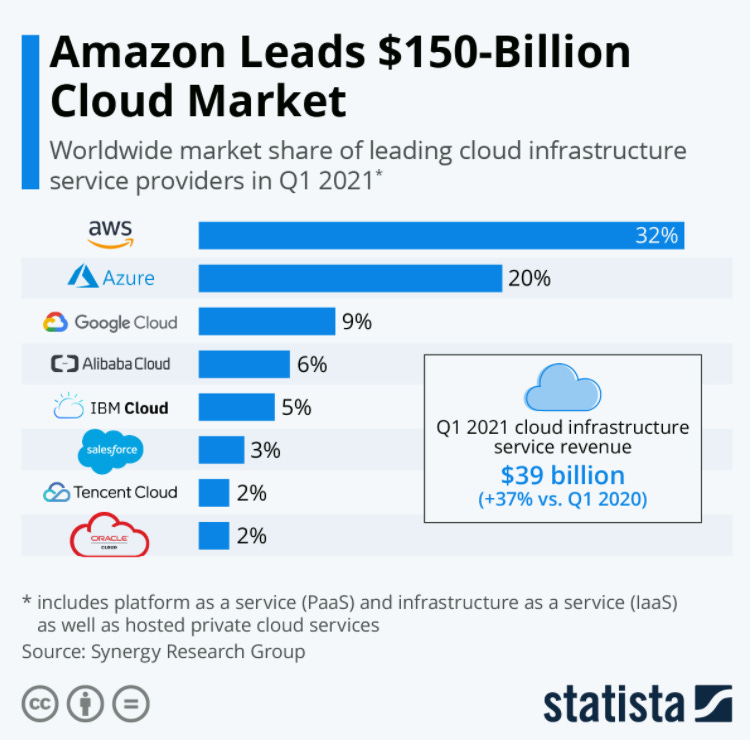

Amazon Web Services (AWS)

The company is the dominant player in the $150 billion cloud industry with a cloud infrastructure service revenue of $39 billion.

Source: Statista

Amazon has maintained its dominant position during the last years with a market share of over 30%. As you can see in the chart below, Azure (Microsoft) and Google Cloud have strongly increased their market share during the last years.

However, while their increase has been magnificent, it has not been at the cost of taking away Amazon’s market share but rather to smaller players. This situation has not prevented Amazon from growing at very high rates and proves its strong know-how, competitive price, and quality service comparing with other rivals.

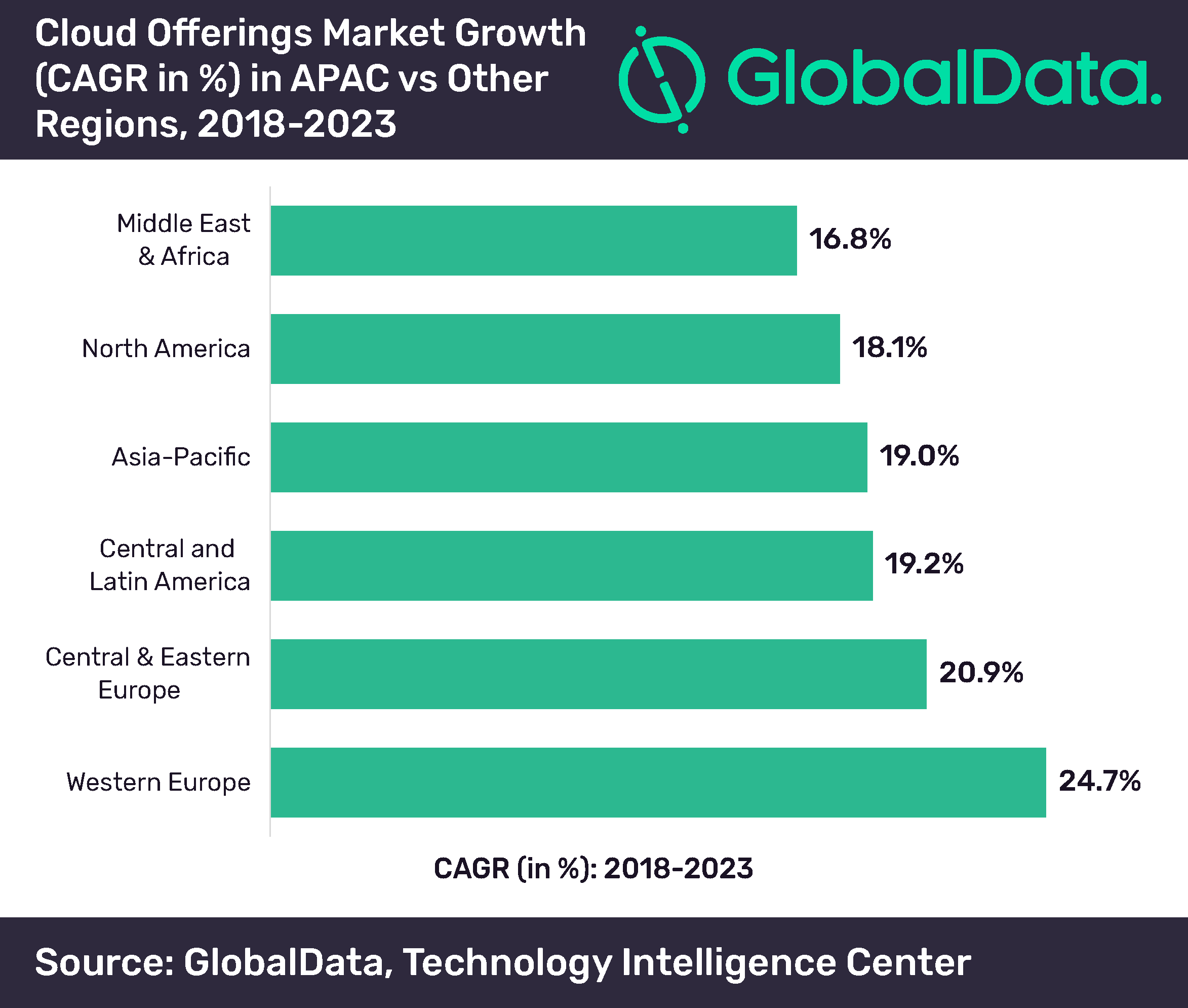

There should be plenty of growth opportunities for all the players in the industry. Forecasts for IaaS and PaaS imply a 25% revenue CAGR between 2020 and 2023 and a market of nearly $200 billion by 2023.

In terms of regions, Europe is expected to experience growth rates over 20% until 2023 whereas North America, a more “mature” market, is expected to experience growth rates of around 18%. The Middle East & Africa will be the region expected to grow the least with rates close to 17%. These growth rates seem pretty amazing to me.

Considering that AWS is the business segment with the highest margins, the expected growth in the cloud services industry for the coming years is great news for Amazon's future.

AWS margins have been around 20%-30% in terms of profitability despite several price reductions in the service along the way.

In the last letter to shareholders, Jeff Bezos revealed that the Amazon Web Services segment that earned $45 billion in revenue in 2020 could easily generate $50 billion or more soon at the current growth rate. AWS is a profit powerhouse.

In Q1 FY21, even though the segment made up just 12% of sales, it commanded a whopping 47% of all operating profits.

Source: Quarterly results

If you apply the operating profit margin of AWS over the last 12 months (30%) to the $50 billion annualized sales, AWS's operating earnings should easily top $15 billion over the next year. For perspective, that's more than the operating profit Amazon generated as a whole in 2019 at $14.5 billion. Amazon’s cloud business line (AWS) is the jewel in the crown.

Furthermore, Amazon's backlog is accelerating its growth. Backlog represents the total value of signed contracts that didn’t get reported as revenue because the agreements run for multiple years. Contracts are usually with large companies to whom they make offers with consequent price cuts. AWS is being aggressive in terms of price cuts, but considering AWS margins, there is nothing to worry about.

As mentioned in the last conference call, AWS had a backlog of future contracts totaling $52.9 billion at the end of Q1 FY21, with a weighted average remaining life of just more than three years.

“That’s up about 55 percent...so it really continues to be really strong,” said David Fildes, Amazon’s director of investor relations. “The momentum we’re seeing in here is a lot of hard work and innovation. You can expect to continue to see customers making these long-term commitments.”

Do you want to know more?

We have just covered three of the many business lines that Amazon has. As you probably can see, Amazon is a monster, and it’s hard to summarize all the information in just one post. In the next article, you will learn about the following segments:

Amazon Subscription Services -> Amazon Prime.

Amazon Physical Stores -> integration of Whole Foods and the opening of Fresh, Go stores.

Other -> includes Amazon Healthcare and Amazon Ads, which I think is one of the most undervalued assets of the company.

Gaming and Twitch

Music and Video

The Amazon Alexa Fund

👉New to the newsletter? Make sure you subscribe here:

👉Help me grow this amazing community: if you enjoyed this post, make sure to share it with anyone who could benefit from it.

If you have any ideas related to the information you’d like to see each week, or perhaps where you feel it could improve, please reply to this email, or drop me a DM on Twitter @buddhist_invest

Thank you for your support, and all the best in your journey to become a successful investor.

Yours truly,

The Buddhist Investor

Disclosure: This information reflects my personal opinion and is merely informative. Therefore it should not serve as a basis for an investment recommendation. Investors must perform a previous due diligence analysis before making investment decisions and be responsible for their actions.