12 Reasons to Buy Facebook Stock and Never Sell

12 Reasons to Buy Facebook Stock and Never Sell

“Our lives are not defined by what we possess, but by what we pursue.”

—The Buddhist Investor

Dear investor,

In the stock market, great opportunities are rare and tend to appear from time to time. when you see an opportunity you need to act quickly and decisively. When the odds are stacked in your favor, you need to invest heavily, because good prices might not come along again soon.

Currently, Facebook occupies 9% of my portfolio, and I have no intention of selling the stock anytime soon. My first contact with Facebook was at the end of 2018 when the Federal Reserve announced that interest rates would increase and the stock market had its worst December since the Great Depression. I first purchased Facebook’s stock at $137-$145 when it was trading for 25 times free cash flow.

Although Facebook stock is trading close to its all-time highs, the company has presented great earnings results, yet its current FCF valuation multiple is around 26 times. Since the current situation in the financial markets remains me a little bit of that of December 2018, I’ve been adding more Facebook stock to my portfolio!

While things could change in the future, here are 12 reasons why I'm so confident it’s a great investment opportunity to own for life and never sell.

It’s a dominant business

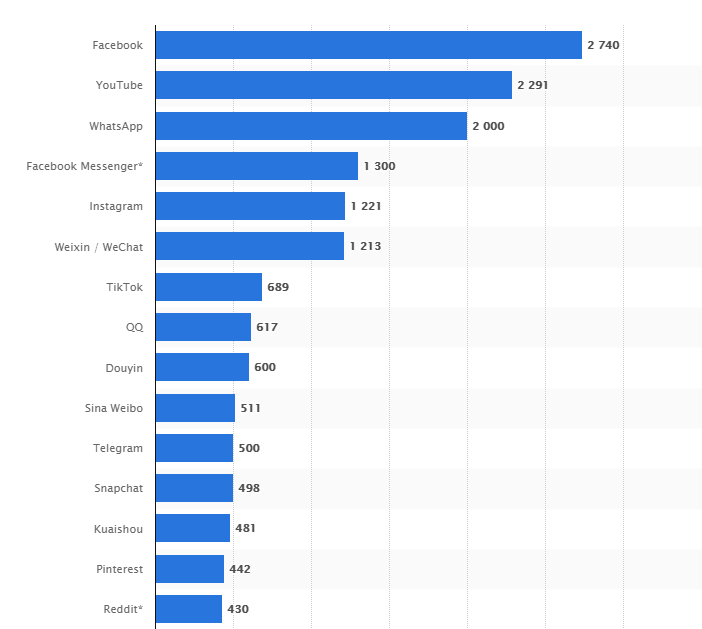

Facebook is the largest social network in the world, with 2.9 billion monthly active users.

Source: FB Earnings Presentation Q1 2021

The company currently also owns four of the biggest social media platforms, all with over 1 billion monthly active users each: Facebook (core platform), WhatsApp, Facebook Messenger, and Instagram. The only platform ranking in the Top 5 that doesn’t belong to Facebook is Youtube.

It’s still a growing business

The growth in users and user engagement and the valuable data they generate makes Facebook attractive to advertisers in the short and long term. The combination of these valuable assets and expected continuing growth in online advertising bodes well for Facebook, as the firm generates strong top-line growth and remains cash flow positive and profitable.

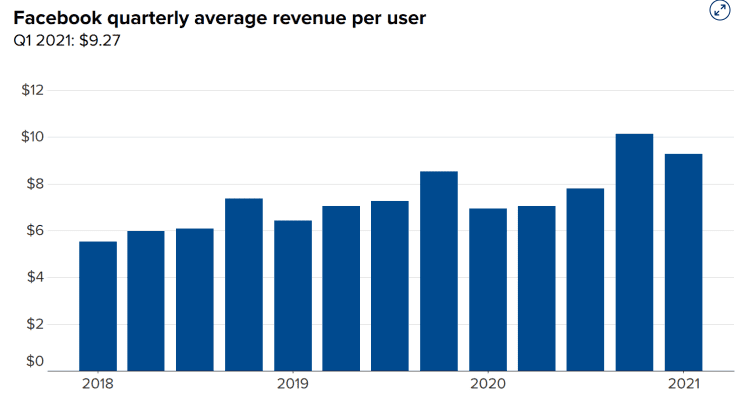

We could forgive Facebook if its growth started to slow markedly. But for a company its size - with a market cap of $889 billion - it still shows robust growth. Facebook’s ad revenue per user is growing, demonstrating the value that advertisers see in working with the firm.

Source: Facebook's average revenue per user (ARPU) from 2012 to 2020 (in U.S. dollars)

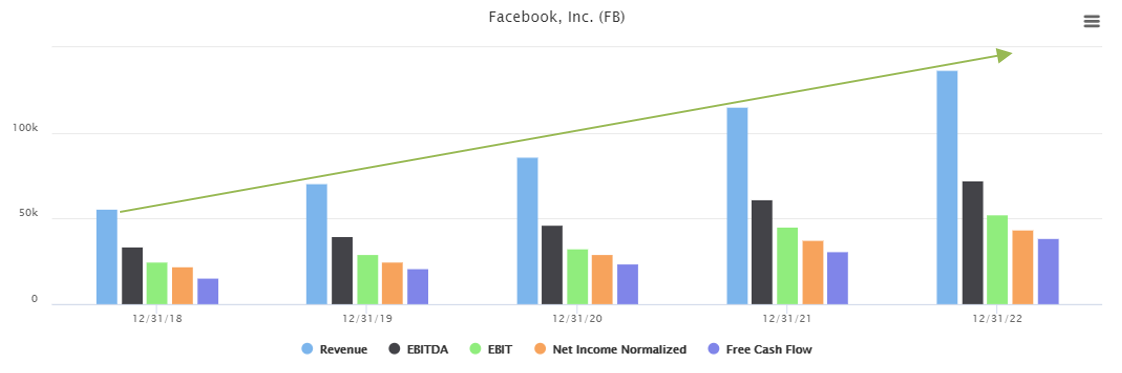

Consider that Facebook’s 2020 total revenue grew 22% to $86 billion, from $71 billion the prior year.

That's simply ridiculous for a company that's already Facebook's size.

Don't forget about WhatsApp or Instagram

The firm’s Facebook app, Instagram, Messenger, and WhatsApp are among the world’s most widely used apps on both Android and iPhone smartphones.

Instagram has already proved to be a gold mine, and we have yet to see how Facebook really plans on monetizing WhatsApp. But what's clear is that both of these subsidiaries are ridiculously popular. Statista estimates that Instagram has around 1.2 billion active users, while WhatsApp has around 2 billion.

Data. So much data.

An evil government organization could spend a century spying on the world's citizens and still just scratch the surface of the type of data that Facebook has. According to eMarketer, on average, users are on Facebook and Instagram a combined 65 minutes per day posting videos and photos, exchanging messages, making comments, uploading content, liking or disliking other content, and more. That's 395 hours per year of the company recording all of your preferences. With access to such data and billions of photos and videos uploaded by its users, Facebook continues to enhance the social network by offering even more relevant content to its users.

This demonstrates the value of the platform to users and its network effect. With more users and usage time than any other social network, Facebook provides the largest audience and the most valuable data for social network online advertising.

Antitrust enforcement and further regulations pose a threat to Facebook's valuable data. However, increased restrictions on data access and usage would apply to all firms, not just Facebook. Privacy concerns have been subjected to much debate over recent years and will continue to be debated in the future. However, I believe convenience over privacy issues online is likely going to win this debate.

This situation has weakened Facebook’s brand. Nevertheless, it’s important to understand that media tends to share unfavorably publications that negatively affect Facebook’s brand. After all, Facebook is one of the biggest competitive threats that traditional media companies have.

Competition? What competition?

Facebook has one of the strongest competitive advantages possible: the network effect. With each person who joins Facebook, those who aren't on the network have the motivation to sign up. Inherently, that makes sense: who would want to go on the site if none of their friends were there?

These network effects serve to both create barriers to success for new social network upstarts (as demonstrated by the firm’s success against Snap), as well as barriers to exit for existing users who might leave behind friends, contacts, pictures, memories, and more by departing to alternative platforms.

In addition, the daily average times spent on those platforms increased during the COVID-19 pandemic, possibly further strengthening Facebook’s network effect moat source.

Over time, users are likely to become further dependent on and spend more time using Facebook and Instagram, which will continue to attract advertisers, resulting in a stronger network effect.

Facebook has also expanded its user base in the growing mobile market, which positively affected the network effect as it became more valuable to advertisers, and resulted in more ad revenue growth.

The main driver behind the growth in online advertising has been the expansion in the mobile ad market and the video ad format. Most Facebook users are now accessing Facebook and its apps via mobile devices.

Its cash reserves provide optionality to the company

As of March 2021, Facebook had around $64 billion in cash and equivalents on hand, versus absolutely no long-term debt. Facebook can use that money to test its more innovative projects, make strategic investments in the next Instagram or WhatsApp, buy back shares, or even eventually start paying a dividend.

The point is that cash gives the company options...no matter the economic climate.

Zuckerberg's just getting started

There aren't many world-beating companies you can invest in that are run by a 37-year-old genius. As long as he doesn't go the Bill Gates route and spend his time on other projects, Zuckerberg could be at the helm for another 30 or 40 years...and that's not even too much of a stretch.

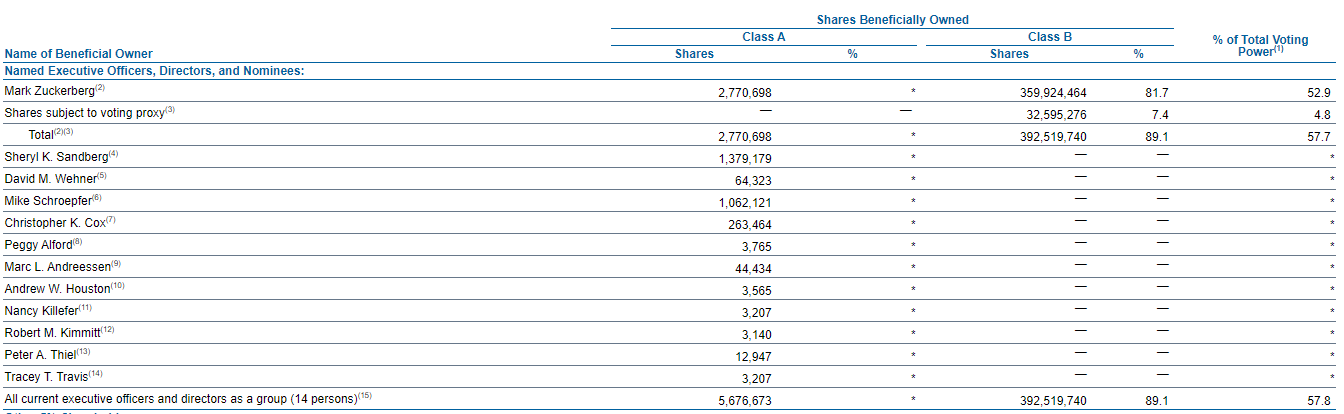

Skin in the game

Mark Zuckerberg's skin is very much in the game. He controls over 395 million shares of Facebook, and his management team collectively - including himself - own over 398 million shares and 57.8% of the company's voting power.

Source: Annual Meeting & Proxy Statement 2021

Facebook Q1 2021 results were astonishing

Here’s how the company fared in the quarter, relative to estimates:

Earnings: $3.30 per share vs. $2.37 per share forecast

Revenue: $26.17 billion vs. $23.67 billion expected

Daily active users (DAUs): 1.88 billion vs. 1.89 billion forecast

Monthly active users (MAUs): 2.85 billion vs. 2.86 billion forecast

Average revenue per user (ARPU): $9.27 vs. $8.40 forecast

The company reported revenue of $26.17 billion for the quarter, which was up 48% compared with a year prior. Facebook’s net income grew 94% to $9.5 billion, from $4.9 billion a year prior.

Facebook attributed the significant increase in revenue to a 30% year-over-year increase in the average price per ad and a 12% increase in the number of ads delivered.

The company announced that this revenue growth is expected to remain stable or accelerate modestly in the 2Q FY21 compared with slower growth a year prior due to the pandemic. Also, the company expects revenue growth in the 3Q FY21 and 4Q FY21 to decelerate to more normalized levels compared with the fast growth experienced during those periods a year prior as a result of the pandemic.

Moreover, Facebook’s “Other” revenue came in at $732 million for the quarter, up 146% compared with last year. That accounted for nearly 3% of Facebook’s revenue in the quarter. This includes sales of Oculus virtual reality headsets and Portal video-chatting devices.

The future looks bright ahead

During the Q1 release, Facebook CEO Mark Zuckerberg talked about the company’s focus on building e-commerce features as a key part of delivering a “personalized” experience to users. Zuckerberg also announced that the company now counts more than 1 billion monthly active users who visit Facebook’s Marketplace service, where users can buy and sell goods.

Also, he explained how building out payment technology, including the digital currency and Novi digital wallet, will be key to enabling more commerce on Facebook’s services.

Zuckerberg also reiterated several new features the company is building for Instagram creators to make money. He said those features will incentivize creators to post more content on Instagram.

Finally, the application of AI technology to Facebook’s various offerings, along with the launch of VR products, will increase user engagement, driving further growth in advertising revenue.

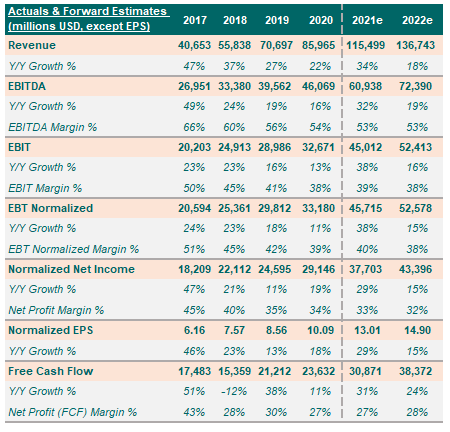

Estimates for the firm are positive

Wall Street forward estimates for 2021 and 2022 are the following ones:

Source: Own elaboration

Estimates for 2021 in comparison with 2020:

Revenue is expected to grow 34%.

EBITDA is expected to grow 32% with an EBITDA margin of 53%.

EBIT is expected to grow 38% with an EBIT margin of 39%.

Normalized net income is expected to grow 29% with a net profit margin of 33%.

Normalized EPS is expected to grow 29%.

Free cash flow is expected to grow 31% with a free cash flow to sales ratio of 27%.

Estimates for 2022 in comparison with 2021:

Revenue is expected to grow by 18%.

EBITDA is expected to grow by 19% with an EBITDA margin of 53%.

EBIT is expected to grow by 16% with an EBIT margin of 38%.

Normalized net income is expected to grow by 15% with a net profit margin of 32%.

Normalized EPS is expected to grow by 15%.

Free cash flow is expected to grow by 24% with a free cash flow to sales ratio of 28%.

Valuation looks attractive

You could be forgiven for thinking you've missed the train on Facebook stock. It is, after all, up 883% from its 2012 levels and also up 44% YTD. However, based on its current attractive valuation and its growth expectations, Facebook stock still has a long way to go.

When looking at Facebook’s valuation multiples, we can see the following information:

EV/Revenues multiple of 7.0x -> Its normalized historical average is 7.0x.

EV/EBITDA of 13.2x-> Its normalized historical average is 13x.

EV/EBIT of 18.1x-> Its normalized historical average is 19x.

P/E of 24.0x-> Its normalized historical average is 24x.

P/FCF of 25.8x-> Its normalized historical average is 30x.

Source: Own elaboration

Facebook's current valuations seem fair valued compared to its historical averages. That’s great news for investors who are looking to buy high-quality businesses at a fair price. Of course, the price could be cheaper, but it would be a mistake to pass on this opportunity just because the valuation isn’t cheap enough. Besides, you can always add to your position if the valuation gets even more attractive.

One of my favorite metrics to use when valuing stocks is the P/FCF ratio. As of 05/19/2021, Facebook stock currently trades for 26 times free cash flow. Although Facebook stock has done absolutely nothing during the last 9 months, ($303 in August 2020 to $313 in May 2021), the business keeps growing and improving its fundamentals.

Consequently, as you can see in the chart below, the multiple has contracted from its peak in August 2020 of 41 times FCF to its current levels of 26 times FCF, offering a really attractive valuation.

Source: Own elaboration

Let’s consider now 3 future possible scenarios in the next 5 years, assuming we buy Facebook’s stock at its current price of $313.59 as of 05/19/2021.

Best case scenario: Facebook’s free cash flows grow at a CAGR of 18% and trades at 30 times free cash flow. This situation would imply a target price of $841 in 2026 with an internal rate of return (IRR) of 22% or 2.7 times your initial investment.

Base case scenario: Facebook’s free cash flows grow at a CAGR of 15% and trades at 25 times free cash flow. This situation would imply a target price of $616 in 2026 with an internal rate of return (IRR) of 14% or almost 2 times your initial investment.

Worst case scenario: Facebook’s free cash flows grow at a CAGR of 13% and trades at 23 times free cash flow. This situation would imply a target price of $497 in 2026 with an internal rate of return (IRR) of 10% or 1.6 times your initial investment.

As you can see, even in the worst-case scenario, investors could potentially achieve returns equal to the S&P 500 historical average return. Seems like the investment provides room for error and a wide margin of safety, and that's why I think you, too, should consider buying - and holding - Facebook shares today.

Risks

Of course, all stock market investments have an element of risk. As most fundamental investors do, my definition of risk has nothing to do with volatility but rather with any external circumstances that could potentially damage Facebook’s moat.

Facebook’s potential risks could be summarized as follows:

Facebook could be affected severely if online advertising no longer grows or if more advertising dollars shift to others like Google or Snapchat.

Its competitive landscape is getting tougher. Despite rapid user growth, many of Facebook’s customers may also belong to other social networks, such as Snapchat or TikTok, so the firm will continually have to fight to capture a user’s time and engagement with its properties.

Antitrust enforcement and further regulations pose a threat to Facebook's valuable data. Regulations could emerge that limit the application and collection of user and usage data, or restrict acquisitions, affecting data utilization and growth.

Remember, you shouldn't buy or sell any stock without first performing your due diligence analysis. Do your homework and research work. Independent thinking is a required skill if you want to become a successful investor.

If you want to perform your analysis, here you have the company’s investor relations link where you can find all the information and reports I’ve used for my investment thesis.

To help me grow this amazing community and if you enjoyed this post, make sure to share it with anyone who could benefit from it.

Thank you for your support, and all the best in your journey to become a successful investor.

Yours truly,

The Buddhist Investor

👉 If you enjoyed reading this post, feel free to share it with friends!

For more like this, make sure to subscribe here:

Disclosure: This information reflects my personal opinion and is merely informative. Therefore it should not serve as a basis for an investment recommendation. Investors must perform a previous due diligence analysis before making investment decisions and be responsible for their actions.