Who Will Stop Amazon?

Who Will Stop Amazon?

Amazon Due Diligence [3/3]

Dear investors,

This is the third and final part of Amazon’s due diligence. The due diligence has been divided into 3 articles. In case you missed the first and second posts, you can find them here: Who Will Stop Amazon? Amazon Due Diligence [1/3] and Who Will Stop Amazon? Amazon Due Diligence [2/3]

Remember, in no case, this information provides a buy or sell recommendation. The content is merely informative and it reflects my personal opinion. Investors should perform their due diligence analysis before making investment decisions.

The Buddhist Investor is a platform, which mainly has an educational purpose. Whether you’re a novel investor or an experienced one, my goal is to help you make better decisions in the stock market and develop a long-term investing mindset.

Now, let’s finish what we started!

Management Skin in the Game

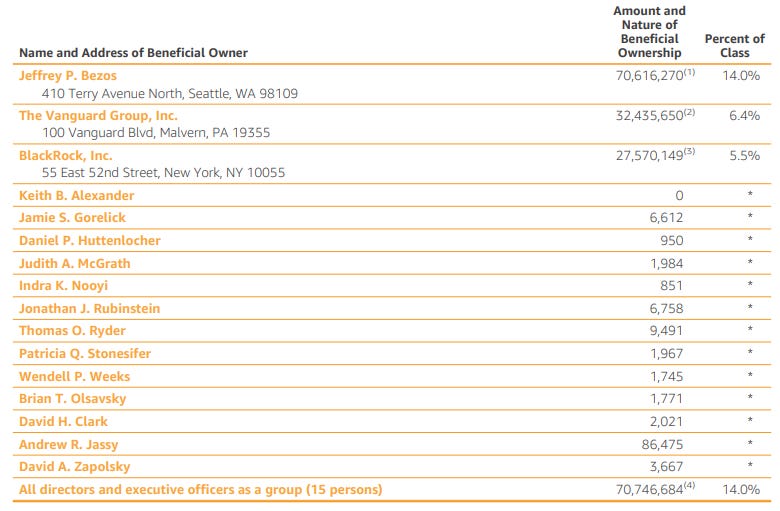

As you probably already know, one of my obsessions when investing in the stock market is looking for businesses that insiders possess a big chunk of the total shares. Insiders owning a high percentage of the total shares outstanding is a guarantee that they will not make stupid decisions that could harm shareholders’ interests.

Of course, the key element is Jeff Bezos, Amazon's founder and executive chair of the company board. He is the company's biggest shareholder, with 70.6 million shares representing 14% of outstanding shares.

Source: Amazon 2021-Proxy-Statement

Bezos was CEO of Amazon since the company was founded and until July 5, 2021, when he stepped down in favor of Andrew Jassy.

In terms of remuneration, Mr. Bezos has a base salary of $81,840 and other annual compensations of $1,600,000. That might seem a lot, but this kind of compensation is very low taking into account he is the executive chair and former CEO of one of the largest companies in the world in terms of market capitalization -> 1.8T

Also, Mr. Bezos has never received any stock-based compensation from Amazon.

It seems clear to me that Jeff Bezos is appropriately incentivized and his interests are appropriately aligned with shareholders’ interests. The main incentive he has to increase his wealth is through the appreciation of the stock, which benefits all shareholders.

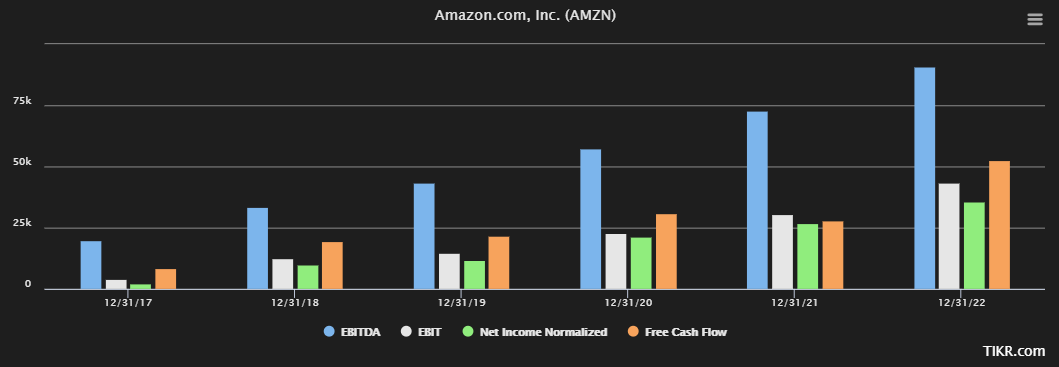

Amazon Q2 2021 Results

Here’s how the company did in the last quarter, relative to estimates:

Earnings: $15.12 per share vs. $12.30 per share forecast

Revenue: $113.08 billion vs. $115.2 billion expected

Source: TIKR.com

The company reported revenue of $113.08 billion for the quarter, which was up 27% compared with a year prior. That’s a significant slowdown from the second quarter of 2020 when sales skyrocketed 41% year over year. However, investors should understand that 2020 was an exceptional year due to the pandemic.

As mentioned by Brian Olsavsky (Amazon CFO), “before COVID-19, we've been growing at a revenue growth rate close to 20%. 2019 full-year growth was 22%. And revenue growth for the first two months of 2020 was 21%. Once the pandemic hit and lockdowns began in March 2020, the initial growth rate jumped into the mid-30% range.”

Therefore, it’s normal to see some slowdown in comparison with 2Q 2020. In my opinion, a growth rate of 27% still seems quite exceptional considering Amazon’s size.

While Amazon’s second-quarter sales disappointed the market, earnings beat expectations, helped by its highly profitable cloud-computing, subscriptions, and advertising businesses. Amazon’s net income grew 48% to $7.8 billion, from $5.2 billion a year prior.

Amazon Web Services (AWS) grew its revenue 37% in the second quarter, faster than 32% growth in the previous quarter. AWS revenue came in at $14.81 billion in the quarter, surpassing analysts’ estimated $14.20 billion. Considering that AWS represents half of the total operating income Amazon generates, a growth rate of 37% is great news for the business.

In addition, Amazon’s “other” unit, which includes advertising and other services, grew revenue 87% year over year during the period.

For the third quarter, Amazon said it expects to book sales between $106 billion and $112 billion, representing growth of 10% to 16% compared to the same period last year. That’s also well below consensus estimates of $119.2 billion.

“Our customers are safe and healthy and ordering from us. And we know that there’ll be more vacations or be more mobility. They’ll be doing things that probably people shied away from last year and that’s all good,” Olsavsky said on the call with reporters. “But it does tend to lead them to do other things besides shop. So we’re just adjusting our run rates in the period that we see that happening.”

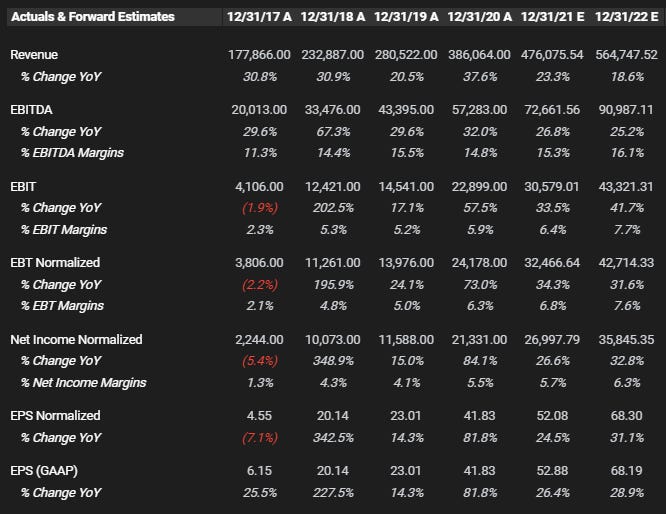

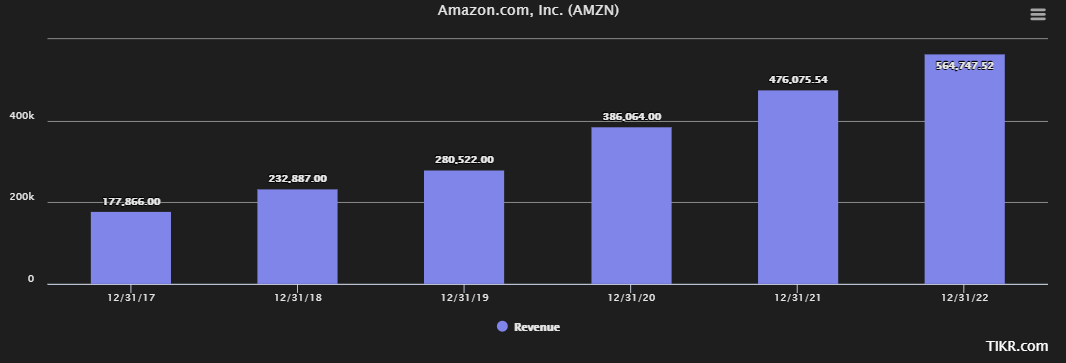

Amazon Forward Estimates

Wall Street forward estimates for 2021 and 2022 are the following ones:

Source: TIKR.com

Wall Street estimates for 2021 in comparison with 2020:

Revenue is expected to grow by 23%.

EBITDA is expected to grow by 27% with EBITDA margins of 15%.

EBIT is expected to grow by 34% with EBIT margins of 6.4%.

Normalized net income is expected to grow by 27% with net income margins of 5.7%.

Normalized EPS is expected to grow by 25%.

Free cash flow is expected to decrease by 10% with a free cash flow to sales ratio of 5.9%. Capex is expected to grow by 25% in comparison with 2020. That’s not necessarily bad news, since Amazon is aggressively reinvesting a big chunk of the cash flow it generates into infrastructure and fulfillment centers to generate additional growth.

Wall Street estimates for 2022 in comparison with 2021:

Revenue is expected to grow by 19%.

EBITDA is expected to grow by 25% with EBITDA margins of 16%.

EBIT is expected to grow by 42% with EBIT margins of 7.7%.

Normalized net income is expected to grow by 33% with net income margins of 6.3%.

Normalized EPS is expected to grow by 31%.

Free cash flow is expected to grow by 88% with a free cash flow to sales ratio of 9.3%. Wall Street analysts expect that during 2022 Amazon will reinvest fewer cash flows into infrastructure and fulfillment centers with Capex increasing only 14% in comparison with 2021 and consequently free cash flow will increase substantially.

The Compounding Power of Amazon

The key financial characteristic of compounders is that they enjoy sustainable, high return on invested capital (ROIC), which is generated by a combination of recurring revenues, high gross margins, and low capital intensity.

This combination helps support strong free cash flow generation that, crucially, must be either reinvested or distributed to shareholders. Any M&A activity should be fully justifiable on ROIC grounds rather than “strategic” or “accretive” grounds at the expense of eroding overall ROIC.

The financial strength of these compounders tends to come from the innovation-driven intangible assets that the companies possess, which, in turn, provide pricing power.

I love to invest in businesses that generate high ROIIC and also with high reinvestment rates. These two variables are key to generate shareholder value over time.

For instance, a company with a high ROIIC but a low reinvestment rate will create much less value in comparison with a similar company that is reinvesting back into the business most of the cash flows it generates.

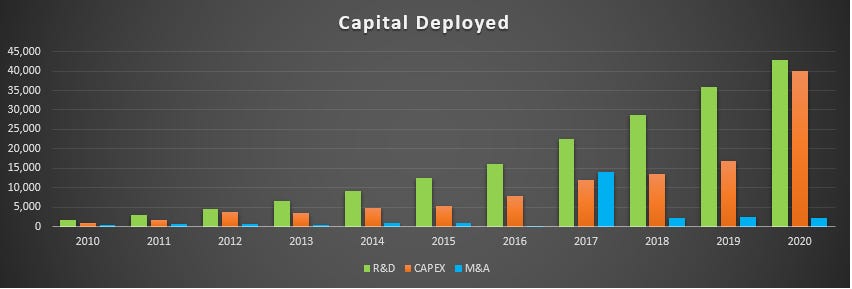

Amazon can reinvest the cash flows it generates through:

R&D -> Innovation

Capex-> Infrascturcutre and fulfillment centers

M&A-> Acquisitions such as Whole Foods, Twitch, MGM, etc.

Here you can see how Amazon distributed its investments and deployed capital since 2010:

Source: Own elaboration

As you can see, most of the cash flow the business generates is deployed to R&D and Capex, and from time to time Amazon executes some important acquisitions.

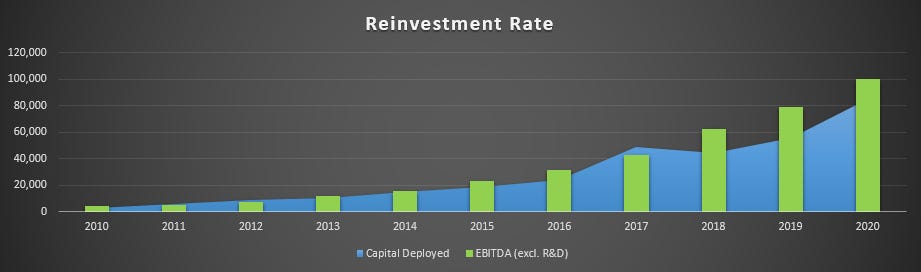

A great check to see if Amazon is generating high ROIIC’s is comparing the total capital deployed with the amount of incremental EBITDA (excluding R&D) that the business generates.

Since 2010, for every $100 of capital invested Amazon generated $39 of EBITDA (excl. R&D) -> That represents a ROIIC of 39%.

Since 2015, for every $100 of capital invested Amazon generated $36 of EBITDA (excl. R&D)-> That represents a ROIIC of 36%.

Since 2017, for every $100 of capital invested Amazon generated $29 of EBITDA (excl. R&D)-> That represents a ROIIC of 29%.

As you can see, the returns are decreasing a little bit. The larger Amazon gets, the harder it is to maintain its high returns. However, it’s important to remember that Amazon’s management has a long-term mindset and some of the important investments of the last few years may take a little longer to yield results. Anyway, these high returns seem quite extraordinary to be ignored.

In addition, Amazon's reinvestment rate has been historically high.

Since 2010, for every $100 of EBITDA (excl. R&D), $83 was reinvested back into the business in form of R&D, Capex, or M&A-> Reinvestment rate of 83%.

Since 2015, for every $100 of EBITDA (excl. R&D), $81 was reinvested back into the business in form of R&D, Capex, or M&A-> Reinvestment rate of 81%.

Since 2017, for every $100 of EBITDA (excl. R&D), $77 was reinvested back into the business in form of R&D, Capex, or M&A-> Reinvestment rate of 77%.

Source: Own elaboration

The fact that Amazon is reinvesting at high rates of returns most of the cash flow the business generates is what has created value to shareholders during the last decade.

As you can see in the chart below, during the last 10 years the stock has generated a 32.1% CAGR, close to the ROIIC the underlying business has generated during that same period.

Source: TIKR.com

As mentioned by Charlie Munger, “Over the long term, it's hard for a stock to earn a much better return than the business which underlies it earns. If the business earns 6% on capital over 40 years and you hold it for that 40 years, you're not going to make much different than a 6% return - even if you originally buy it at a huge discount. Conversely, if a business earns 18% on capital over 20 or 30 years, even if you pay an expensive-looking price, you'll end up with one hell of a result.”

Valuation Looks Fair

When looking at Amazon’s valuation multiples, we can see the following information:

EV/Revenues multiple of 3.3x -> Its 5Y historical average is 3.1x.

EV/EBITDA of 21x-> Its 5Y historical average is 23x.

P/FCF of 41x-> Its 5Y historical average is 35x.

Source: Own elaboration

Amazon's current valuations don’t seem too attractive compared to its historical averages. It doesn’t seem expensive either but rather fair valued. For anyone looking to invest for the long term in an excellent business like Amazon, paying a “fair” price is not a bad deal. Of course, the price could be cheaper, but in the future, you can always add to your position if the valuation gets more attractive.

My favorite metric to use when valuing stocks is the P/FCF ratio. As of 08/01/2021, Amazon stock currently trades for 41 times FCF.

As you can see in the chart below, the multiple has contracted from its peak in August 2020 of almost 50 times. However, I agree with you, 41 times is not precisely a low multiple.

Given Amazon’s high quality and expected growth, paying anything below 33 times FCF would be a great price to pay. The lower the better of course.

Source: TIKR.com

Let’s consider now 3 future possible scenarios in the next 5 years, assuming we buy Amazon’s stock at its current price of $3,327.59 as of 08/01/2021.

Best case scenario: Amazon’s free cash flow grows at a CAGR of 20% and the stock trades at 33 times FCF. This situation would imply a target price of $6,645 in 5 years with an internal rate of return (IRR) of 15% or 2.0 times your initial investment.

Base case scenario: Amazon’s free cash flow grows at a CAGR of 18% and the stock trades at 30 times FCF. This situation would imply a target price of $5,554 in 5 years with an internal rate of return (IRR) of 11% or 1.7 times your initial investment.

Worst case scenario: Amazon’s free cash flow grows at a CAGR of 15% and the stock trades at 27 times FCF. This situation would imply a target price of $4,395 in 5 years with an internal rate of return (IRR) of 6% or 1.3 times your initial investment.

As you can see, the first two scenarios offer decent returns, 15%, and 11% respectively. These returns are above or close to the S&P 500 historical average return -> 10%

However, the worst scenario offers a potential return of only 6%, well below the S&P 500 historical average. Analyzing the 3 scenarios seems like the investment provides some margin of safety but it’s not too wide.

I don’t think buying Amazon today would be a huge mistake if you plan to hold the stock for many years. In the same way, waiting for a more attractive valuation wouldn’t be a mistake either. Every investor should act according to their needs and their long-term plan.

Business Risks

Of course, all stock market investments have an element of risk. As most fundamental investors do, my definition of risk has nothing to do with volatility but rather with any external circumstances that could potentially damage Amazon’s moat.

Amazon’s potential risks could be summarized as follows:

Regulatory concerns are rising for large technology firms, including Amazon. Further, the firm may face increasing regulatory and compliance issues as it expands internationally.

New investments, notably in fulfillment, delivery, and AWS should dampen free cash flow growth. Currently, new investments are generating additional value to the business but at some point, this positive situation could change. Also, Amazon’s penetration into some countries might be harder than in the U.S. due to inferior logistic networks.

Covering too many different products or markets could be a mistake. The bets on Amazon Music, Amazon Video, and the like, at the moment, do not have too much of a view to succeed. Amazon's purpose indeed is to offer an attractive package, not the product separately.

Amazon may not be as successful in penetrating new retail categories, such as luxury goods, due to consumer preferences and an improved e-commerce experience from larger retailers.

A slowdown in AWS could seriously affect the total operating profit of the company since AWS generates half of it.

Jeff Bezos’ departure should not affect too much considering the company’s size, but it is clear that he has been a key figure in Amazon’s evolution.

Remember, you shouldn't buy or sell any stock without first performing your due diligence analysis. Do your homework and research work. Independent thinking is a required skill if you want to become a successful investor.

If you want to perform your analysis, here you have the company’s investor relations link where you can find part of all the information and reports I’ve used for my investment thesis.

👉New to the newsletter? Make sure you subscribe here:

👉Help me grow this amazing community: if you enjoyed this post, make sure to share it with anyone who could benefit from it.

If you have any ideas related to the information you’d like to see each week, or perhaps where you feel it could improve, please reply to this email, or drop me a DM on Twitter @buddhist_invest

Thank you for your support, and all the best in your journey to become a successful investor.

Yours truly,

The Buddhist Investor

Disclosure: This information reflects my personal opinion and is merely informative. Therefore it should not serve as a basis for an investment recommendation. Investors must perform a previous due diligence analysis before making investment decisions and be responsible for their actions.