Top 12 Cognitive Biases That Cause Investment Mistakes

Top 12 Cognitive Biases That Cause Investment Mistakes

“Investing is the intersection of economics and psychology.”

—Seth Klarman

Dear investor,

We tend to think that our brain is a perfect machine. The reality is that our brain is definitely powerful, but it has its weaknesses.

Behavioral psychologists experts call such weaknesses “biases.” They define them as gaps in our reasoning abilities that can spoil our decision-making. While it’s impossible to eliminate mental biases, we can avoid mistakes that our biases cause by just taking notice of them.

Simply noticing these gaps isn’t enough. If you know how your biases can hurt you, you will take precautionary actions to safeguard yourself from them.

We’ve all seen movies where a thief wears a police uniform to pass through a security checkpoint. The real police officers assume that because the person is wearing a uniform like theirs, they must be a real police officer. That’s an example of a cognitive bias.

What does a fake cop have to do with your investment choices? Actually, investors do the same types of assumptions that may or may not necessarily be true. In the stock market, biases are not an exception. Even the most perceptive investors, armed with years of market experience, can fall prey to mental biases that lead to poor investment decisions.

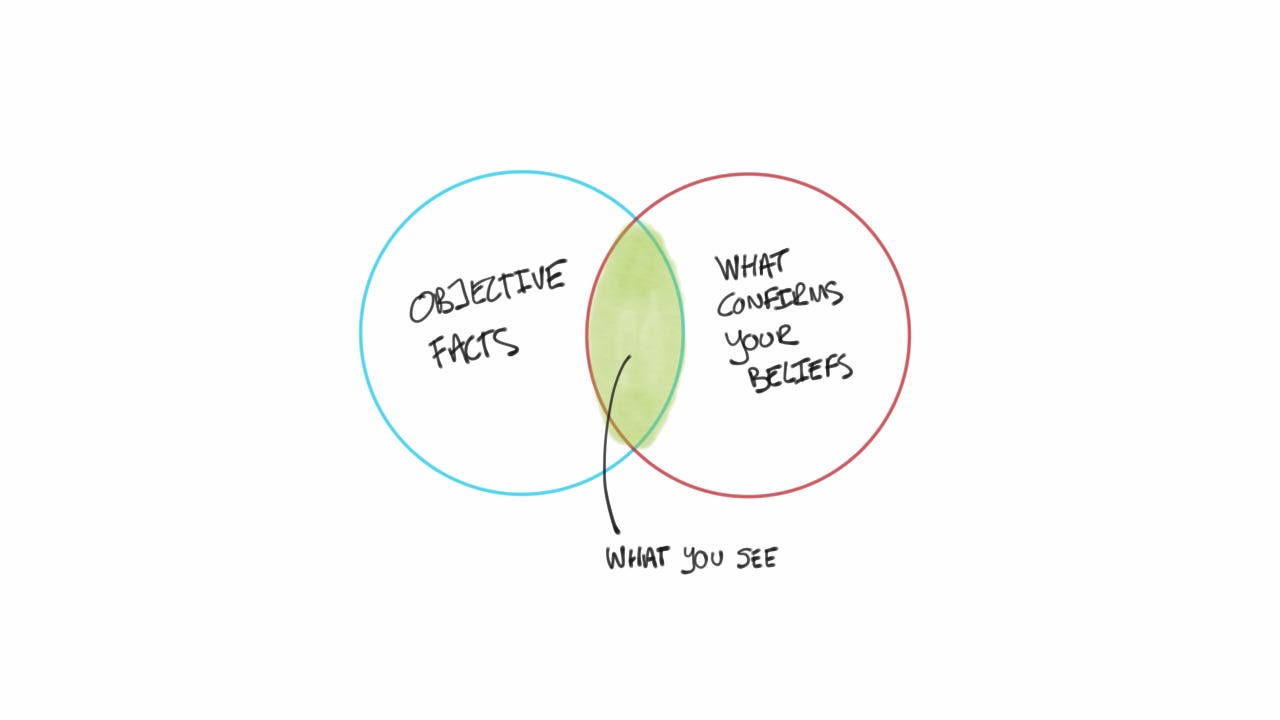

Confirmation Bias

Have you noticed that you put more weight into the opinions of those who agree with you? Investors do this too. How often have you analyzed a stock and later researched reports that supported your thesis instead of seeking out arguments that may contradict your opinion?

To minimize the risk of confirmation bias attempt to challenge the status quo and seek information that causes you to question your investment thesis. Charlie Munger, the Vice-Chairman of Berkshire Hathaway and Warren Buffett’s business partner, said: “Rapid destruction of your ideas when the time is right is one of the most valuable qualities you can acquire. You must force yourself to consider arguments on the other side.”

Gambler's Fallacy

Let’s assume that the S&P 500 has closed to the upside five trading sessions in a row. Now you believe chances are high that the market will drop on the sixth day. While it may happen, on a purely statistical basis, the past events don’t connect to future events. There may be other reasons why the sixth day will produce a down market, but the fact that the market is up five consecutive days is irrelevant.

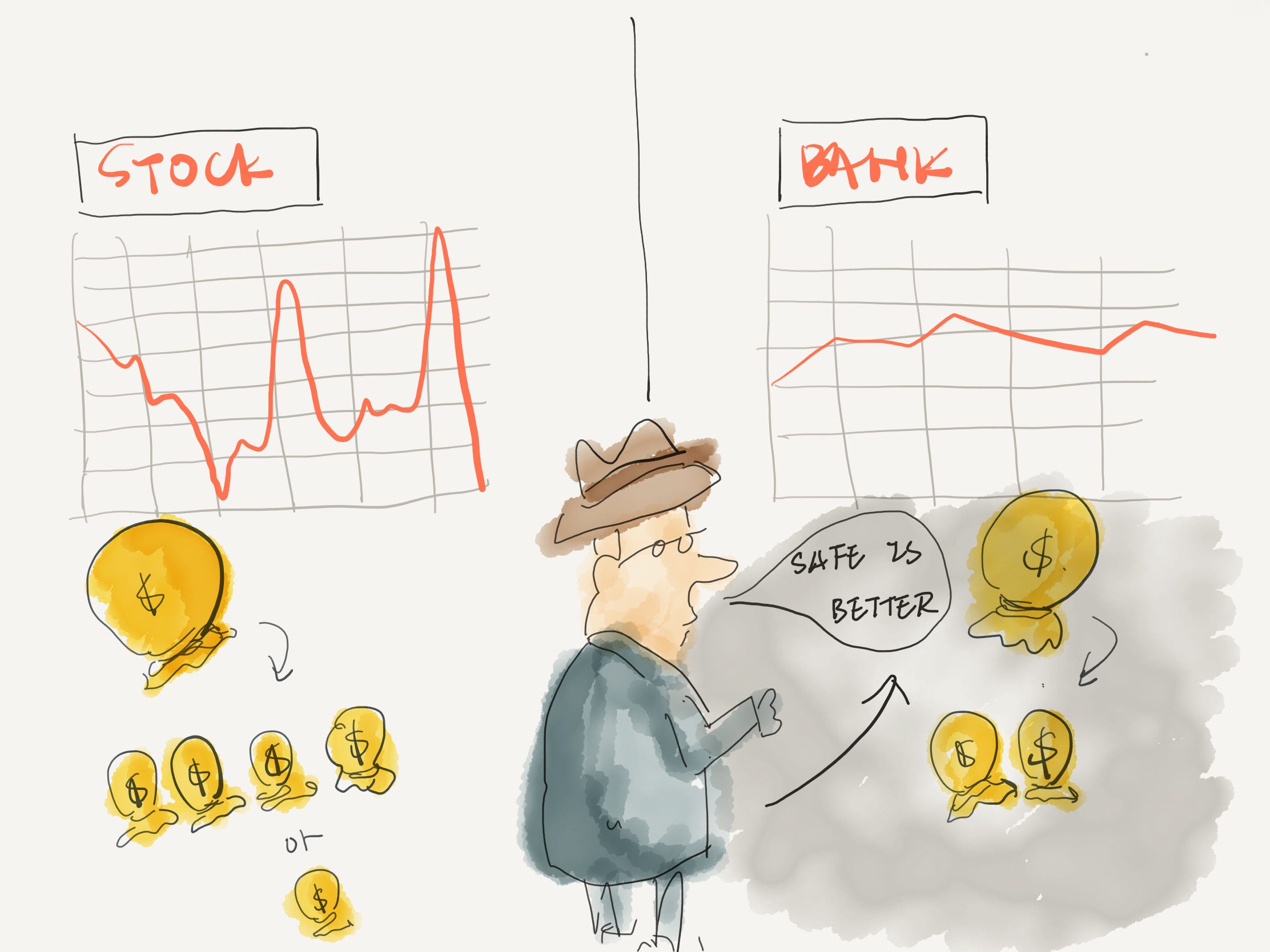

Risk-Averse Bias

The bull market is alive and strong, yet many investors have missed the rally because of the fear that it will reverse course. Risk-averse bias often causes investors to put more weight on bad news than good news. These types of investors typically overweigh safe, conservative investments and look to these investments more actively when markets are uncertain.

This bias can potentially cause the effects of risk to hold more weight than the possibility of reward. The famous investor Peter Lynch said: “Far more money has been lost by investors trying to anticipate corrections than lost in the corrections themselves.”

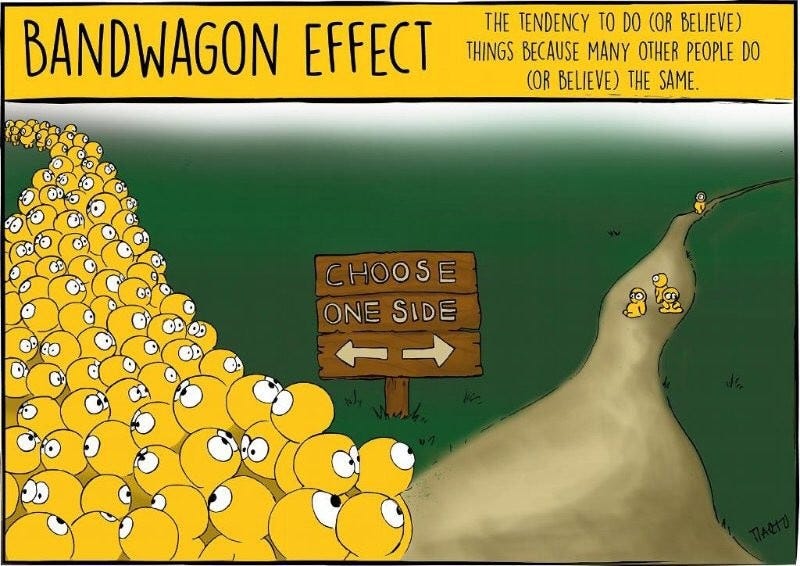

Bandwagon Effect

Warren Buffett became one of the most successful investors in the world by resisting the bandwagon effect. His famous advice to be greedy when others are fearful and fearful when others are greedy is a denouncement of this bias. Going back to confirmation bias, investors feel better when they are investing along with the crowd. But as Buffett has proven, an opposite mentality, after exhaustive research, may prove more profitable.

To be a successful investor, you must be able to analyze and think independently. Speculative bubbles are typically the result of groupthink and herd mentality. Don’t find comfort in the fact that other people are doing certain things or that people agree with you. At the end of the day, you will be right or wrong because your analysis and judgment are either right or wrong.

In avoiding the pitfalls of the bandwagon effect, I’m reminded of the Robert Frost poem, The Road Not Taken, where he writes: “Two roads diverged in a wood and I, I took the one less traveled by. And that has made all the difference.”

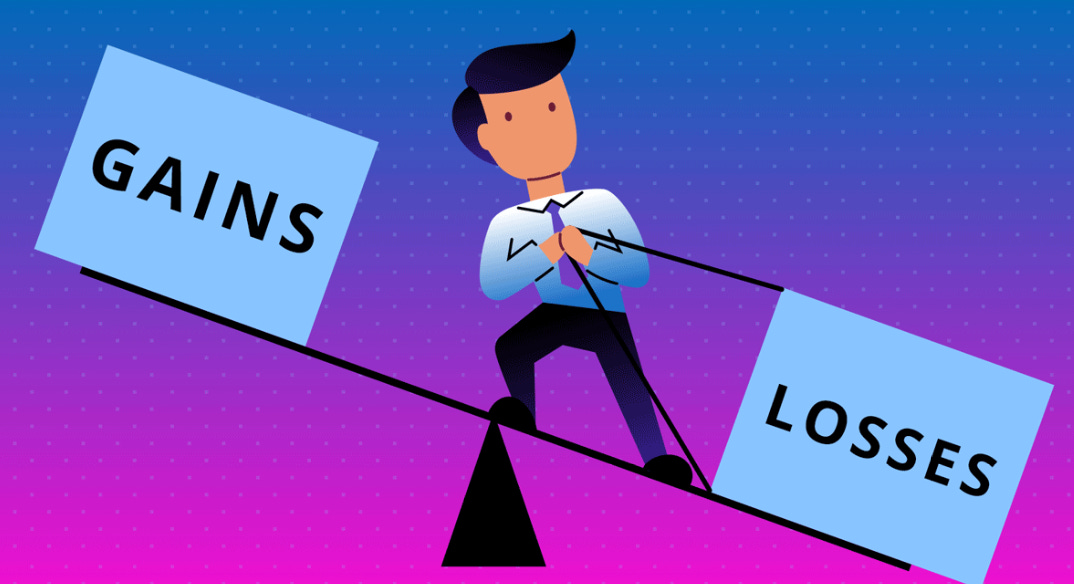

Loss-Aversion Bias

Do you have a stock in your portfolio that is down so much that you can’t stomach the thought of selling? In reality, if you sold the stock, the money that is left could be reinvested into a higher-quality stock. But because you don’t want to admit that the loss has gone from a computer screen to real money, you hold on in hopes that you will, one day, make it back to even.

All past decisions are sunk costs and a decision to retain or sell an existing investment must be measured against its opportunity cost. To minimize the risk of loss-aversion bias, you have to focus on the opportunity cost of retaining an existing investment versus making a new investment in the portfolio.

Many investors would make superior investment decisions if they constrained the number of investments in their portfolios as they would be forced to measure opportunity cost and make choices between investments.

Buffett often gives the illustration that investors would achieve superior investment results over the long term if they had an imaginary punch card with space for only 20 holes and every time they made an investment during their lifetime they had to punch the card. In Buffett’s view, this would force investors to think carefully about the investment, including the risks, which would lead to more informed investment decisions.

Overconfidence Bias

“I have an edge that you and others don’t have.” A person with overconfidence bias believes that their skill as an investor is better than others' skills. Take, for example, the person who works in the pharmaceutical industry. They may believe in having the ability to invest within that sector at a higher level than other investors. The market has made fools out of the most respected investors. It can do the same to you.

To avoid overconfidence bias, trade less and invest more. Understand that by entering into trading activities you're trading against computers, institutional investors, and others around the world with better data and more experience than you.

The odds are overwhelmingly in their favor. The only edge individual investors have is their time frame. Institutional investors need to provide outstanding short-term returns in a highly competitive industry in order to keep their jobs, but you don’t have to. Just invest for the long-term. Don’t waste your biggest advantage and resist the urge to believe that your information and intuition are better than others in the market.

Regret bias

Admit it, you've done this at least once. You were confident that a certain stock was value-priced and had very little downside potential. You put the trade on but it slowly worked against you. Still feeling like you were right, you didn't sell when the loss was small. You let it go because no loss is a loss as long as you don't sell the position. It continued to go against you but you didn't sell until the stock lost a big chunk of its value.

Behavioral economists call it, regret. As humans, we try to avoid the feeling of regret as much as possible, and often we will go to great lengths, sometimes illogical lengths, to avoid having to own the feeling of regret. By not selling the position and locking in a loss, investors don’t have to deal with regret. Research shows that investors were 1.5 to 2 times more likely to sell a winning position too early and a losing position too late, all to avoid the regret of losing gains or losing the original cost basis.

Limited Attention Span

There are thousands of stocks to choose from but the individual investor has neither the time nor the desire to research each. Humans are constrained by what economist and psychologist Herbert Simon called, "bounded rationality." This theory states that a human will make decisions based on the limited knowledge they can accumulate. Instead of making the most efficient decision, they'll make the most satisfactory decision.

Because of these limitations, investors tend to consider only stocks that come to their attention through websites, financial media, friends, and family, or other sources outside of their own research. For example, if a certain biotech stock gains FDA approval for a blockbuster drug, the move to the upside could be magnified because the reported news catches the eye of investors. Smaller news about the same stock may cause a very little market reaction because it doesn't reach the media.

In order to avoid this bias, recognize that the media has an effect on your investing activities. Learning to research and evaluate stocks that are both well-known and “off the beaten path” might reveal lucrative trades that you would have never found if you waited for them to come to you.

For instance, I tend to own in my portfolio a combination of well-known large stocks and not widely known small-cap stocks. Don't let media noise impact your decisions. Instead, use the media as one data point among many.

Be extremely selective about the blogs your read, the Twitter accounts you follow, the podcasts you listen and the videos you watch. Media and news generate noise, which is the enemy of equanimity and the friend of bad decisions.

Chasing Trends

This is arguably the strongest investing bias. Researchers on behavioral finance found that 39% of all new money committed to mutual funds went into the 10% of funds with the best performance the prior year. Although financial products often include the disclaimer that “past performance is not indicative of future results,” retail traders still believe they can predict the future by studying the past.

Humans have an extraordinary talent for detecting patterns and when they find them, they believe in their validity. When they find a pattern, they act on it but often that pattern is already priced in. Even if a pattern is found, the market is far more random than most investors care to admit. One study from The University of California found that investors who weighted their decisions on past performance were often the poorest performing when compared to others.

If you identify a trend, it's likely that the market identified and exploited it long before you. You run the risk of buying at the highs. If you want to exploit an inefficiency, take the Warren Buffett approach: “Be fearful when others are greedy and be greedy when others are fearful.” Following the herd rarely produces large-scale gains.

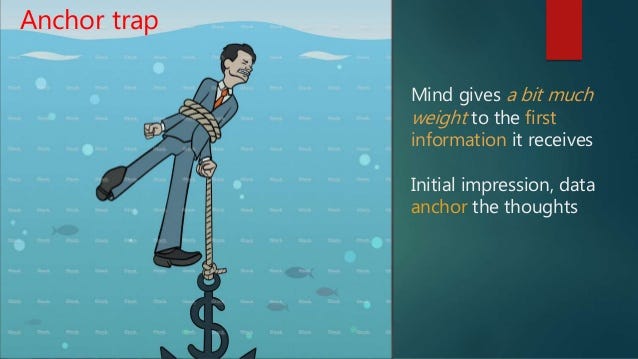

Anchoring bias

Anchoring bias is the tendency to rely too heavily on, or anchor to, a past reference or one piece of information when making a decision. There have been many academic studies undertaken on the power of anchoring in decision-making. Studies typically get people to focus on items such as their year of birth or age before being asked to assign a value to something. The studies show that people are influenced in their answer, or anchored, to the random number that they have focused on prior to being asked the question.

From an investment perspective, one obvious anchor is the recent share price. Many people base their investment decisions on the current share price relative to its trading history. In fact, technical analysis bases investing on charting share prices. Unfortunately, where a share price has been in the past presents no information as to whether or not a stock is cheap or expensive.

Also, investors tend to use as a reference point, the price they paid for a stock. Unfortunately, the stock market doesn’t care about the price you initially paid. Investors should base their investment decisions on whether or not the share price is trading at a discount to their assessment of intrinsic value and forget about past share prices.

Hindsight bias

Hindsight bias is a tendency to see beneficial past events as predictable and bad events as not predictable. In recent years, we have read many explanations for poor investment performance that blame the unpredictability and volatility of markets. However, unpredictable events are by definition not predictable and investors should put all their energy only on the things they can control.

For instance, during the lockdown, many of the stocks I own in my portfolio such as Amazon, Facebook, Google, Microsoft, etc., skyrocketed because of their condition of tech companies. During the lockdown, tech companies were the ones that saved us. Otherwise, the situation could have been even worst.

Did I anticipate these increases? Of course not. I don’t have a crystal ball. It was an unpredictable event and I just got lucky. Sure, I had previously identified the strengths and high qualities of these businesses but the sudden increase in their stock price was just a stroke of luck.

Mistakes shouldn’t be attributed to an unpredictable event or market volatility but rather to errors of judgment. It is important that as much as we recognize the role of luck in success, the role of risk means we should forgive ourselves and leave room for understanding when assessing failures. Nothing is as good or as bad as it seems.

To reduce hindsight bias, try to spend significant time upfront setting out in writing the investment case for each stock, including your estimated return. This makes it more difficult to ‘rewrite’ your investment history with the benefit of hindsight.

The Illusion of Control

This occurs when we tend to overestimate our ability to control events or outcomes. People can behave as if chance events are accessible to personal control. A simple form of this effect is found in casinos: when rolling dice in a craps game people tend to throw harder when they need high numbers and softer for low numbers.

Not all investors believe that they have complete control. However, a lot of them do believe that they have some influence over the market. In most cases, this is not true because investment markets are huge markets where trillions of dollars change hands every week. Hence, if an individual investor or even a small to mid-size institution believes that they are in control of the market, they may be wrong.

Is true that some of the investor’s predictions might come true in the short-run. However, it may be a mere co-incidence and may not prove anything in the long-run. A lot of times, investors feel in control of their portfolios because they use techniques such as limit orders, stop losses, etc., to buy and sell shares. Also, “fancy” spreadsheets may create a sense of control over your investment idea or portfolio. However, in many cases, it just leads to unnecessary buying and selling as prices fluctuate within a given range. The illusion of control bias is also closely linked to the feeling of overconfidence, which has been discussed in this article.

To be a successful investor over the long term, you can mitigate biases by understanding and identifying them. Cognitive biases are “hard-wired” and we are all liable to take shortcuts, oversimplify complex decisions and be overconfident in our decision-making process.

Understanding our cognitive biases can lead to better decision-making, which is fundamental to lowering risk and improving investment returns over time.

To help me grow this amazing community and if you enjoyed this post, make sure to share it with anyone who could benefit from it.

Thank you for your support, and all the best in your journey to become a successful investor.

Yours truly,

The Buddhist Investor

👉 If you enjoyed reading this post, feel free to share it with friends!

For more like this, make sure to subscribe here:

Dear Sir your article is Very logic and thoughtful and your search on the market just like preach of Buddha's.