Goeasy Q2 2021 Earnings Review

Dear investors,

Last week, Goeasy Ltd. reported record results for Q2 FY21. The first two quarters of 2021 have been extraordinary for the company.

Currently, Goeasy is the largest position in the BI Portfolio with a percentage of 10.6%. Since I first purchased the stock at $42 CAD, the price has increased more than +330%, or 4.3 times the initial investment.

My portfolio risk management strategy is simple. I just let the winners run. The companies have to earn the right to be in the TOP positions. That’s what exactly happened with Goeasy, which clearly deserves to be the largest position in the BI Portfolio.

Despite the great returns, the path hasn’t been easy. When the COVID-19 crisis started back in March 2020, the stock price dropped more than 63% from 79 CAD to 29 CAD. If during the crash I had sold my position, today we wouldn’t be talking about Goeasy.

To succeed as an investor, it’s really important to control your emotions, especially during panic selloffs. You should never sell a security based on fear but rather on reasoned analysis.

Source: Goeasy stock information

But before we start to analyze the latest results, let’s inquire a little bit deeper about what the company does.

Let’s get started with it!

Business Overview

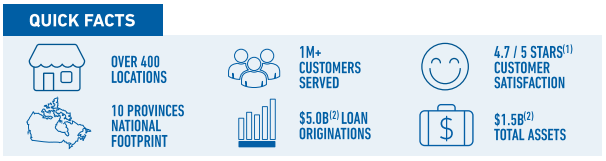

Goeasy provides loans and other financial services to consumers in Canada. It also leases household products to consumers. Goeasy main focus is in the non-prime consumer credit market with a potential addressable market of $28.6B. Currently, Goeasy market share only accounts for 4%. It’s a really fragmented market and the potential to grow is huge.

The company operates through two segments:

Easyfinancial: represents the most significant and profitable segment of the company since it generates 78% of total revenues with an operating margin of 47.6%. This business line provides unsecured and real estate secured installment loans, and secured saving loans. It also offers loan protection plans, and several optional home and auto benefits products.

Easyhome: generates 22% of total revenues with a lower operating margin in comparison with Easyfinancial of only 22%. This business line leases furniture, appliances, electronics, and computers.

In 2006, the company launched Easyfinancial, and from that moment the less profitable segment Easyhome lost business relevance in favor of Easyfinancial.

As of December 31, 2020, Goeasy operated 266 easyfinancial locations that include 14 kiosks, as well as 161 easyhome stores that include 35 franchises. The company was formerly known as easyhome Ltd. and changed its name to goeasy Ltd. in September 2015.

Source: Company reports

Record Results for the Second Quarter

During the quarter, the Company experienced an increased level of demand within its direct-to-consumer lending channels, aided by strong growth in its point-of-sale finance channel.

Increased originations and loan growth, complemented by improved credit performance and the April 30, 2021 closing of the previously announced acquisition of LendCare Holdings Inc. (“LendCare”), led to record financial results.

“The second quarter was highlighted by a significant increase in loan originations, continued strength in the credit performance of our portfolio, and the expansion of our point-of-sale lending channel through the acquisition of LendCare,” said Jason Mullins, Goeasy’s President and CEO, “As we have now entered a period of accelerated growth, revenues lifted 34%, while adjusted diluted earnings per share rose 38%.

Key Takeaways from Q2:

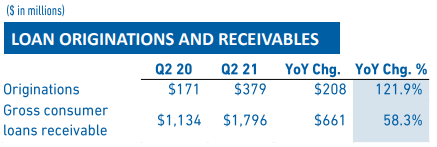

Loan Portfolio of $1.80 billion, up 58%

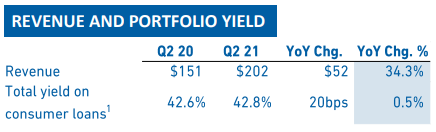

Revenue of $202 million, up 34%

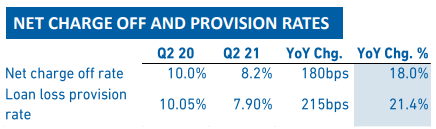

Net Charge Off Rate of 8.2%, down from 10.0%

Adjusted Quarterly Net Income of $43.7 million, up 50%

Adjusted Quarterly Diluted Earnings per Share of $2.61, up 38%

Securitization Facility Increased from $200 million to $600 million, with an interest reduction of 110 bps.

Improving demand and credit performance led to record results for the company.

Where did the Origination of Growth come from?

Record loan originations: the Company generated a record $379 million in total loan originations in the second quarter, up 122% compared to the $171 million produced in the second quarter of 2020, and a sequential increase of 39% from the $272 million in loan originations in the first quarter of 2021.

LendCare acquisition: the deal is expected to accelerate growth through additional product range offerings and point-of-sale channel expansion. To finance the acquisition of LendCre, the company completed a $173M public equity offering and US$320M 4.375% senior unsecured notes issuance in April 2021.

Was April a great moment to issue new stock to finance part of the LendCare acquisition despite the potential dilution that it may cause?

I certainly think it was. The stock price was trading at ATH and valuation multiples were well above their historical average. In my opinion, management did a smart move.

Omnichannel strategy: so far is providing great results. Point-of-sale and digital platforms are driving new customers growth.

In addition to the approximately $445 million gross consumer loan portfolio acquired through the acquisition of LendCare, the increase in loan origination volume led to organic growth in the loan portfolio of an additional $74 million during the quarter, resulting in a total gross consumer loan receivable portfolio of $1.80 billion, up 58% from $1.13 billion as at June 30, 2020.

The growth in consumer loans led to an increase in revenue, which was a record $202 million in the quarter, up 34% over the same period in 2020.

Source: Company reports

Structurally Improved Credit Performance

During the quarter, the Company also continued to experience strong credit and payment performance. When combined with the combination of the structurally lower credit risk of the LendCare portfolio, the net charge-off rate for the second quarter was 8.2%, compared to 10.0% in the second quarter of 2020.

As a result of the continued improvement in underlying credit quality, the improving economic recovery, and the amalgamation of LendCare, the Company reduced its overall allowance for future credit losses to 7.90% from 9.88% in the prior quarter.

Also, following the LendCare acquisition, 32.8% of consumer loan portfolio is now secured, up from 11.1% in Q2 2020. This significant increase improves the overall credit quality of the business.

Source: Company reports

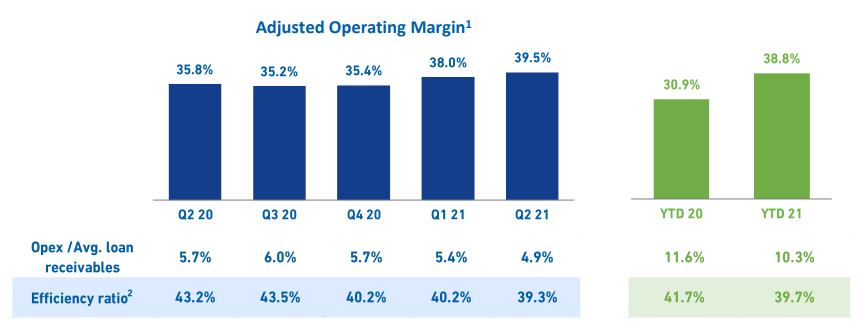

Profitability

Operating income for the second quarter of 2021 was $56.1 million, up 4% from $54.0 million in the second quarter of 2020. The operating margin for the second quarter was 27.7%, down from 35.8% in the prior year.

After adjusting for items related to the acquisition of LendCare and an unrealized fair value loss on investments recorded in the quarter, the company reported record adjusted operating income of $79.9 million, up $25.9 million or 48% over the second quarter of 2020.

Adjusted operating margin for the second quarter was 39.5%, up from 35.8% in Q2 2020. The business achieved increasing operational leverage from scale and lower credit losses.

Source: Company reports

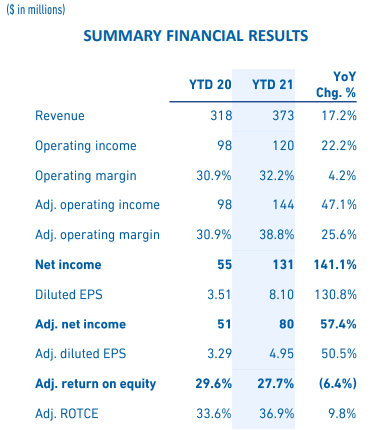

Net income in the second quarter was $19.5 million, compared to $32.5 million in the same period of 2020, which resulted in diluted earnings per share of $1.16, compared to $2.11 in the second quarter of 2020.

After adjusting for non-recurring and unusual items on an after-tax basis, adjusted net income was a record $43.7 million, up 50% from $29.1 million in 2020, resulting in adjusted diluted earnings per share of $2.61, up 38% from $1.89 in the second quarter of 2020.

ROE during the quarter was 12.0%, compared to 37.0% in the second quarter of 2020. After adjusting for the non-recurring and unusual items previously noted, adjusted ROE was 26.9% in the quarter, compared to adjusted ROE of 33.1% in the same period of 2020.

I love when management focuses on financial metrics such as ROE or ROIC. It’s something that not many management teams do and I think is extremely relevant when assessing business performance.

Maintaining Strong Balance Sheet and Significant Liquidity

Key Highlights:

The company upsized the revolving securitization warehouse facility by $400M to a total of $600M and lowered the cost of borrowing by 110bps. The facility is collateralized by a portion of its consumer loans.

Goeasy increased its liquidity to approximately $870M, enough to fund organic growth through Q4 2023.

At Q1 2021, the weighted average cost of borrowing was reduced to 4.8%, down from 5.1% in the prior year.

Net leverage of 64% continues to run lower than their target leverage ratio of 70%. Management is very strict when it comes to net leverage compliance ratios.

Source: Company reports

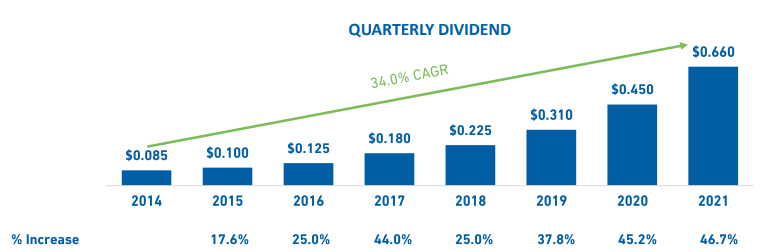

Dividend Friendly

Goeasy paid a quarterly dividend of $0.66 resulting from improved earnings in 2020 and confidence in continued growth.

2021 marks the 17th consecutive year of paying a dividend and the 7th consecutive year of increase in the dividend.

Source: Company reports

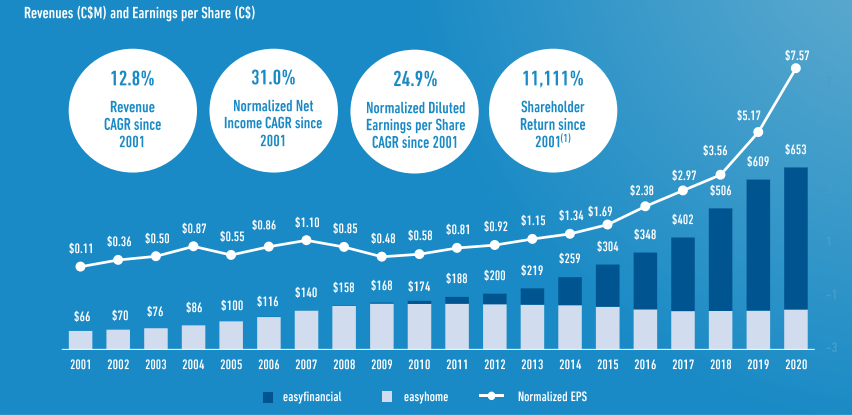

19 Consecutive Years of Revenue Growth and Profitability

From 2001 to 2020, revenue growth and profitability have been extraordinary.

Revenue CAGR: +12.8%

Normalized Net Income CAGR: +31%

Normalized Diluted Earnings per Share: +24.9%

Shareholder Return: +11,111%

Source: Company reports

Future Outlook

Goeasy wants to build Canada’s best-performing non-prime lending platform. As mentioned by the management, they are in the early stages of product, channel, and geographic expansion.

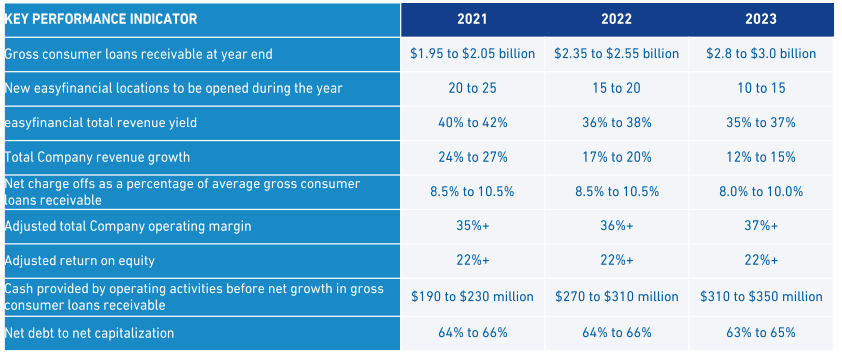

The Company has provided a new 3-year forecast for the years 2021 through 2023. They continue to pursue a long-term strategy that includes expanding its product range, developing its channels of distribution, and leveraging risk-based pricing, which increases the average loan size and extends the life of its customer relationships.

As such, the total yield earned on its consumer loan portfolio will gradually decline, while net charge-off rates moderate and operating margins will expand.

The forecasts outlined below only considers the Company’s expected domestic organic growth plan and don’t include the impact of any future mergers or acquisitions, or the associated gains or losses associated with its investments.

“With the economic recovery underway, the launch of our new auto loan product and the rapid expansion of our point-of-sale platform, we expect the growth of our portfolio to accelerate as we capture a larger share of the $200 billion non-prime consumer credit market,” said Mr. Mullins,

“Our updated three-year forecast reflects growing our consumer loan book to nearly $3 billion by the end of 2023, while gradually reducing the cost of borrowing for our consumers, improving the underlying credit performance and expanding our margins through operating leverage. We remain focused on our goal of becoming the largest and best-performing non-prime consumer lender in Canada, while continuing to deliver market-leading returns for our shareholders.”

Here you can see management forecasts for the next 3 years:

Source: Company reports

Expectations for the Second Half of 2021

For the third and fourth quarters of 2021, total revenue is expected to grow above 35% QoQ whereas normalized net income is expected to grow above 30% QoQ.

For the full year 2021, revenue is expected to grow between 25%-27% YoY whereas normalized net income is expected to grow above 45% YoY. Also, normalized EPS is expected to be close to $10.50 CAD per share.

In addition, management gave the following guidance for Q3 2021:

Gross consumer loan portfolio growth will be between $100M and $120M.

The total yield on loan portfolio will be between 40% and 41%.

The net charge-off rate is expected to be between 8.5% and 9.5%

In my opinion, it seems like during the second half of 2021, the business performance will follow the positive trend of the recent years before the COVID-19 crisis emerged.

👉New to the newsletter? Make sure you subscribe here:

👉Help me grow this amazing community: if you enjoyed this post, make sure to share it with anyone who could benefit from it.

If you have any ideas related to the information you’d like to see each week, or perhaps where you feel it could improve, please reply to this email, or drop me a DM on Twitter @buddhist_invest

Thank you for your support, and all the best in your journey to become a successful investor.

Yours truly,

The Buddhist Investor

Disclosure: This information reflects my personal opinion and is merely informative. Therefore it should not serve as a basis for an investment recommendation. Investors must perform a previous due diligence analysis before making investment decisions and be responsible for their actions.